Coda Octopus (CODA)

Cash-rich, real-time, 3D sonar leader hitting an inflection point with rising naval defense spend, new AR HUD goggles, and UUV demand.

Coda Octopus is a micro-cap, market leader in the niche of real time underwater 3D sonar. At a 17x TEV / FCF, no debt, and $37M (44% of market cap) in net cash equivalents, there is downside protection. There is significant upside from increased naval defense spend, their new DAVD product line, rising demand for unmanned underwater vehicles (UUV’s), and potential acquisitions. Heavy insider ownership.

Background

Coda is the leader in the niche of real time underwater 3D imaging. Coda can be broken down into its sonar vision products (Marine Technology Business), its service (Marine Engineering Business), and its acoustic sensors/materials businesses (i.e. Precision Acoustics Limited (PAL)).

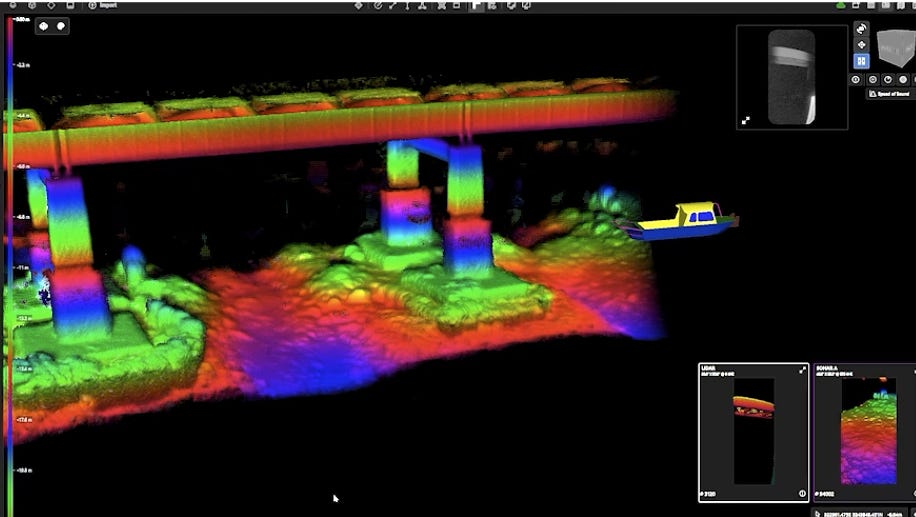

Coda’s main product is the Echoscope. The Echoscope provides real time 3D seeing and measuring in zero visibility conditions underwater. The Echoscope is highly specialized to a number of end use commercial and military applications. Some commercial end uses include port and bridge construction, offshore renewable construction, port channel clearance, and ship hull inspection. Military end uses primarily center around avoiding obstacles during point A to B travel of underwater vehicles. The Echoscope is also available for rent and can be used in tethered dives. Rentals account for ~7% of revenue.

The Echoscope product suite is heavily patented with ~20 patents granted with expiries through 2042. The closest competitors are only able to take static images which take days to render into 3D images. The only other alternatives are 2D sonar which is not adequate for many applications.

One recent developing tailwind is US and foreign navies’ interest in next-generation underwater defense vehicles. These vehicles span from 85 foot long, 85 ton submarines to one-person systems. These are used for mine countermeasures, anti-submarine warfare, and surveillance/reconnaissance missions. To address the trend towards smaller system use cases, Coda has been developing the NanoGen series of their Echoscope. Some NanoGen models are around the size of an iPhone! This is a serious technological feat considering the size of the Echoscope box today. This especially applies to unmanned underwater vehicles (UUV) which is a market expected to grow from $4.8B in 2024 to $11.1B in 2030. The reality here is that underwater warfare is evolving and becoming more complex. Anduril is developing the Ghost Shark for Australia, BAE is developing the Herne, China is developing the AJX002, Helsing is developing the SG-1, Russia has the Vityaz-D, etc. Consider how much warfare is conducted today using remotely controlled UAVs. The same shift is just beginning underwater, and Coda is the only provider of mission critical, real-time 3D, underwater sight.

Most dives are conducted in low to zero visibility conditions. The Diver Augmented Vision Display System (DAVD) is a specialized diver goggle AR HUD built initially for the US Navy divers in these low/zero vis conditions. DAVD has been in development since 2019 with continual testing, iteration, and funding from the US Navy. DAVD provides a real time 3D visual of the diver’s environment, life support data, and digital communications with topside in the diver’s goggles. This is a groundbreaking technology that showcases Coda’s R&D capabilities and laser focus on their niche. The untethered variant launched commercially in 2025 with 16 orders in Q1. This first batch is primarily being used in field trials for use cases like explosive ordinance disposal in the US. Coda is also in talks with two foreign navies interested in equipping their divers with DAVD.

The Marine Engineering Business is basically a subcontractor to prime defense contractors and provides engineering services to help in building large mission critical defense systems. It accounts for ~30% of Coda’s revenue but much less of its income (~10%) as it is lower margin than the products business. This business is vital however as it helps to maintain and establish a strong relationship with the US Navy and generates high margin Echoscope sales.

The acoustics business (i.e. Precision Acoustics Limited) manufactures devices that measure ultrasound from 40 kHz to 50 MHz. Coda acquired PAL on Oct 29th, 2024 for ~$6M cash. In H1 2025, PAL contributed $729k EBT.

Discussion and Valuation

Some structural points in Coda’s favor are its relatively small niche, time to market is 4-5 years of trials for military contracts (e.g. DAVD), and patent portfolio. Their commercial solutions are heavily customized to end use case as well. For instance, it took four years to develop a customized version of their Echoscope for ship hull scanning.

Over the last 4 years, Coda has averaged ~$3M in FCF with very little variance. This speaks to the breadth of end markets they sell into. Adding in PAL gets us another ~$1M in FCF. TEV comes out to around $65M, so ~16 TEV/FCF. Coda has very little in fixed assets, mostly tied up in their buildings, so maintenance capex is <$1M per year. These qualitative and quantitative factors already present a reasonably valued microcap stock with underwater defense spending tailwinds. This is a nice safety margin.

One of the major upside optionalities I want to focus on is the DAVD product commercialization. This is a unique product with a strong value prop for the 3,845 US Navy Seals and also for foreign navies, two of which completed key trials in September 2023. The CTO mentioned on the Q2 earnings call that in total there are 14,000 divers whose needs could be met with the untethered DAVD system across US Special Forces, DoD, US Army, Marine Corps, US Coast Guard, first responders, and law enforcement. DAVD retails for $80k without the Echoscope. Not every DAVD will have an Echoscope, but with the Echoscope, the combined package is likely around $300k.

It’s anyone’s guess the rate of adoption of this product by the US or foreign navies, but some back of the envelope math can suggest that this is a very large market ($500M+ total cumulative sales assuming 1 in 4 DAVD’s has an Echoscope and 100% US Navy Seal adoption) they would have a monopoly in. From management’s Q1 2023 comments on 15% US Navy Seal (i.e. 3845 * 15% Seals) adoption over 5 years, this would add ~$9M in annual income ($15M revenue * 65% gross * 10% tax). Clearly this estimate turned out to be wrong since the first untethered shipments only started in Q1 2025, but this gives some idea on the impact strong DAVD adoption can have on the bottom line. If you take something more bullish like 50% adoption of the quoted 14,000 users over 10 years and 25% of sales including an Echoscope, you get to some insane FCF numbers north of $50M annually, which would send shares to $40+.

Another form of upside optionality is the application of the Echoscope to UUV’s through new specialized product offerings like the Nanogen. This was only recently announced on the Q2 2025 earnings call. I estimate 10-40 small UUV’s produced per year for the US Navy over the next 5 years. The US Navy already bought 21 HII Remus UUV’s in 2024 and 13 in 2025 for the Lionfish system, so this seems reasonable. If they all are equipped with the new Nanogen offering, which I estimate is $50k-100k per unit (complete guess based on sensor count ratios * echo price), this is $500k-$4M in additional revenue and $325k-$2.6M in incremental FCF. Note that this doesn’t include foreign navies or the expected increase in UUV spend over the next 6+ years. This is all pretty speculative, but it could be a nice bump in the core business.

Management is heavily incentivized and shareholder aligned. The CEO, Annmarie Gayle, owns 20% of all shares. Cumulatively all directors and officers own around 30% of all shares. The result is that there is little opportunity for funds to open a position with limited float and $200k average daily volume. As mentioned in the 2023Q4 earnings call, Coda does not wish to engage in share buybacks to worsen this liquidity issue.

In summary, I view Coda as a reasonably cheap, strong niche microcap with multiples of “free” additional upside optionality as DAVD adoption accelerates and NanoGen/Echoscope ride the tailwinds of unmanned underwater vehicle (UUV) defense spend.

Risks

Bad M&A with existing cash balance

US Navy and other foreign navies do not get the budget for DAVD or they get it many years later

Competing products enter the market

Catalyst

DAVD gets traction with US or foreign navies

Value additive acquisition in their niche (e.g. PAL)

Brand building efforts and improving investor outreach

NanoGen/Echoscope adoption in UUV’s + increasing defense spend on UUV’s

Disclaimers

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.